Popular Posts: 5 Software Stocks to Buy Now10 Best “Strong Buy” Stocks — CSGP CONN LL and more5 Pharmaceutical Stocks to Buy Now Recent Posts: 5 Stocks With Ugly Earnings Momentum — FNBN COB NAV SGK LGCY 21 Commercial Banking Stocks to Buy Now 10 Best “Strong Buy” Stocks — CSGP TYL FLT and more View All Posts

Popular Posts: 5 Software Stocks to Buy Now10 Best “Strong Buy” Stocks — CSGP CONN LL and more5 Pharmaceutical Stocks to Buy Now Recent Posts: 5 Stocks With Ugly Earnings Momentum — FNBN COB NAV SGK LGCY 21 Commercial Banking Stocks to Buy Now 10 Best “Strong Buy” Stocks — CSGP TYL FLT and more View All Posts This week, 21 Commercial Banking stocks are improving their overall ratings on Portfolio Grader. Each of these stocks is rated an “A” (“strong buy”) or “B” overall (“buy”).

Pinnacle Financial Partners, Inc. (NASDAQ:) is bumping up its rating from a C (“hold”) to a B (“buy”) this week. Pinnacle Financial Partners is a holding company for Pinnacle National Bank. In Portfolio Grader’s specific subcategory of Earnings Revisions, PNFP also gets an A. .

This week, Taylor Capital Group, Inc. (NASDAQ:) is showing good progress as the company’s rating jumps from a B (“buy”) last week to an A (“strong buy”). Taylor Capital Group is a bank holding company for Cole Taylor Bank. .

This is a strong week for BSB Bancorp, Inc. (NASDAQ:). The company’s rating climbs to B from the previous week’s C. BSB Bancorp operates as a bank holding company. .

BNC Bancorp (NASDAQ:) improves from a C to a B rating this week. BNC Bancorp offers products and services to individuals and small- to medium-sized local businesses. .

This week, Wells Fargo & Company’s (NYSE:) ratings are up from a C last week to a B. Wells Fargo provides financial services in mainly wholesale banking, mortgage banking, consumer finance, equipment leasing, agricultural finance and commercial finance. .

PacWest Bancorp (NASDAQ:) shows solid improvement this week. The company’s rating rises from a C to a B. PacWest Bancorp is the holding company for Pacific Western Bank. The stock price has risen 11% over the past month, better than the 1.3% decrease the Nasdaq has seen over the same period of time. .

U.S. Bancorp’s (NYSE:) ratings are looking better this week, moving up to a B from last week’s C. U.S. Bancorp provides banking and financial services. .

Huntington Bancshares Incorporated (NASDAQ:) is seeing ratings go up from a C last week to a B this week. Huntington Bancshares is a multi-state bank holding company. .

Independent Bank Corp.’s (NASDAQ:) ratings are looking better this week, moving up to a B from last week’s C. Independent Bank is the holding company for Rockland Trust. .

This week, First Financial Bankshares, Inc. (NASDAQ:) pushes up from a C to a B rating. First Financial Bankshares is a multi-bank holding company. .

Pacific Continental Corporation (NASDAQ:) boosts its rating from a B to an A this week. Pacific Continental Bank is a bank holding company that provides commercial banking, financing, and mortgage lending in parts of Washington state and Oregon. .

This is a strong week for First Community Bancshares, Inc. (NASDAQ:). The company’s rating climbs to B from the previous week’s C. First Community Bancshares is the holding company for First Community Bank. .

Top Penny Stocks To Invest In Right Now

Bryn Mawr Bank Corporation (NASDAQ:) gets a higher grade this week, advancing from a C last week to a B. Bryn Mawr Bank offers a full range of personal and business banking services. .

Banco de Chile Sponsored ADR (NYSE:) shows solid improvement this week. The company’s rating rises from a C to a B. NonactiveBanco de Chile provides a wide customer base of individuals and corporations with general banking services. The stock has a dividend yield of 3.3%. .

BOK Financial Corporation (NASDAQ:) earns a B this week, jumping up from last week’s grade of C. BOK Financial provides a range of financial services to commercial and industrial customers, other financial institutions, and consumers in the United States. .

Glacier Bancorp, Inc. (NASDAQ:) improves from a C to a B rating this week. Glacier Bancorp is a regional multi-bank holding company providing commercial financial services to individuals and corporations. .

This week, Washington Trust Bancorp, Inc.’s (NASDAQ:) ratings are up from a C last week to a B. Washington Trust offers a range of financial services to individuals and businesses, including wealth management. .

The rating of First Connecticut Bancorp, Inc. (NASDAQ:) moves up this week, rising from a C to a B. First Connecticut Bancorp operates as the holding company for Farmington Bank that provides consumer and commercial banking services to businesses, individuals, and governments in central Connecticut. .

This is a strong week for First Financial Holdings, Inc. (NASDAQ:). The company’s rating climbs to A from the previous week’s B. South Carolina Bank and Trust is a bank holding company that provides retail and commercial banking, mortgage lending, consumer finance loans, and trust and investment services. .

Canadian Imperial Bank of Commerce (NYSE:) is seeing ratings go up from a C last week to a B this week. Canadian Imperial Bank of Commerce is a global financial institution that serves clients through CIBC retail markets and wholesale banking. The stock’s dividend yield is 3.6%. .

The Bank of Nova Scotia (NYSE:) boosts its rating from a C to a B this week. Bank of Nova Scotia offers various personal, commercial, corporate, and investment banking services in Canada and internationally. The current dividend yield is 2.4%. .

Louis Navellier’s proprietary Portfolio Grader stock ranking system assesses roughly 5,000 companies every week based on a number of fundamental and quantitative measures. Stocks are given a letter grade based on their results — with A being “strong buy,” and F being “strong sell.” Explore the tool here.

AFP/Getty Images How happy were markets that Washington made a deal? Almost as happy as the Afghanistan soccer team after beating Pakistan in August.

AFP/Getty Images How happy were markets that Washington made a deal? Almost as happy as the Afghanistan soccer team after beating Pakistan in August.  Alamy From clothes to car repairs, things just seem to cost more in the winter. Add in holiday shopping, and even the most carefully-planned household budget can get crushed under the weight. But the winter months don't have to wreck havoc on your budget. We talked to the experts to find out how to plan for, and avoid, some common expenses. Season-Proof Your Wardrobe Back when seasons were predictable, switching out one wardrobe for another was a quarterly ritual. But now, there's no reason to invest year after year in winter clothes. A few, well-chosen, high-quality items can blend with fall and spring clothes for a year-round look. And heavy, and expensive winter coats? One or two will do. Ken Downing, the fashion director of Neiman Marcus, says, "We seldom have prolonged exposure to the elements these days. Many of us go from our homes to our cars to our offices. There's really no need for the sort of heavy layers we used to need." The same idea goes for a winter-only wardrobe. Skip buying heavy sweaters only practical a few weeks or months. Downing favors pieces that can be dressed up or down, or layered over, throughout the year. "I love seeing basic essentials like a nice dress or classy skirt and blouse, that work year-round, and can be dressed up with that season's color and accessory." For this fall, Downing recommends leopard accessories like a purse or heels, a belt or a scarf. Get a Jump-Start on Car Problems Bill Tatler, a Firestone mechanic in Brick, N.J., says that certain parts of a car are more likely to fail during the cold months, especially as a car repeatedly goes from being parked in below-freezing conditions to its standard operating temperature. "A battery will almost always go in the winter," Tatler says. "Hoses that are a little worn out should be replaced, because the changes in the temperature could cause them to blow." Tatler recommends coating windshields with a water repellent like Rain-X to help prevent ice from sticking to them, topping off windshield wiper fluid often, and replacing wiper blades. (It's not necessary to replace the arms.) If windshield wipers stop working altogether, it's probably just a blown fuse, which is easy and inexpensive to replace. For drivers of pick-up trucks, Tatler says, "Leave the snow in the bed. The extra weight will add some stability in cold weather, and when it gets warmer, and road conditions improve, the snow will naturally melt away." It may not be ideal for gas mileage, but that load of snow could mean the difference between a slide and an accident. You've Got to Give (a Little!) It's tempting to go overboard when holiday shopping for loved ones, but a bit of caution can save your from a budget blow-out. Skip the ultra-trendy items in favor of an "investment" piece; for example, a leather handbag for a new college graduate or an interview-appropriate tie for a jobseeker. Don't be afraid to ask what people want; sometimes the best gift is something that's truly needed. Alternatively, focus on creating memories rather than giving material items. Gift certificates to a movie (with enough included for popcorn), a night out for two, or a weekend away with the family (or from them!) will last much longer than the memory of a sweater that's pushed into the back of a closet, and never seen again.

Alamy From clothes to car repairs, things just seem to cost more in the winter. Add in holiday shopping, and even the most carefully-planned household budget can get crushed under the weight. But the winter months don't have to wreck havoc on your budget. We talked to the experts to find out how to plan for, and avoid, some common expenses. Season-Proof Your Wardrobe Back when seasons were predictable, switching out one wardrobe for another was a quarterly ritual. But now, there's no reason to invest year after year in winter clothes. A few, well-chosen, high-quality items can blend with fall and spring clothes for a year-round look. And heavy, and expensive winter coats? One or two will do. Ken Downing, the fashion director of Neiman Marcus, says, "We seldom have prolonged exposure to the elements these days. Many of us go from our homes to our cars to our offices. There's really no need for the sort of heavy layers we used to need." The same idea goes for a winter-only wardrobe. Skip buying heavy sweaters only practical a few weeks or months. Downing favors pieces that can be dressed up or down, or layered over, throughout the year. "I love seeing basic essentials like a nice dress or classy skirt and blouse, that work year-round, and can be dressed up with that season's color and accessory." For this fall, Downing recommends leopard accessories like a purse or heels, a belt or a scarf. Get a Jump-Start on Car Problems Bill Tatler, a Firestone mechanic in Brick, N.J., says that certain parts of a car are more likely to fail during the cold months, especially as a car repeatedly goes from being parked in below-freezing conditions to its standard operating temperature. "A battery will almost always go in the winter," Tatler says. "Hoses that are a little worn out should be replaced, because the changes in the temperature could cause them to blow." Tatler recommends coating windshields with a water repellent like Rain-X to help prevent ice from sticking to them, topping off windshield wiper fluid often, and replacing wiper blades. (It's not necessary to replace the arms.) If windshield wipers stop working altogether, it's probably just a blown fuse, which is easy and inexpensive to replace. For drivers of pick-up trucks, Tatler says, "Leave the snow in the bed. The extra weight will add some stability in cold weather, and when it gets warmer, and road conditions improve, the snow will naturally melt away." It may not be ideal for gas mileage, but that load of snow could mean the difference between a slide and an accident. You've Got to Give (a Little!) It's tempting to go overboard when holiday shopping for loved ones, but a bit of caution can save your from a budget blow-out. Skip the ultra-trendy items in favor of an "investment" piece; for example, a leather handbag for a new college graduate or an interview-appropriate tie for a jobseeker. Don't be afraid to ask what people want; sometimes the best gift is something that's truly needed. Alternatively, focus on creating memories rather than giving material items. Gift certificates to a movie (with enough included for popcorn), a night out for two, or a weekend away with the family (or from them!) will last much longer than the memory of a sweater that's pushed into the back of a closet, and never seen again. Bloomberg IBM's revenue falls short of analysts' targets.

Bloomberg IBM's revenue falls short of analysts' targets.  Earnings Wall

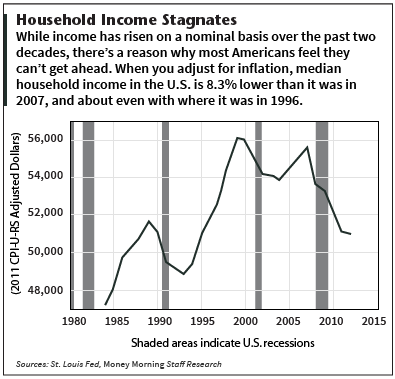

Earnings Wall  What increases Americans have gotten over the years - about $11,000 since 2000 - have been more than negated by inflation.

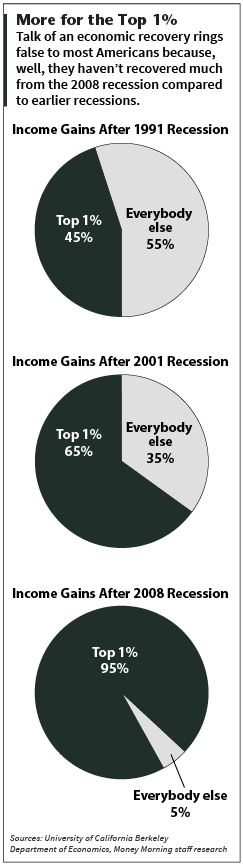

What increases Americans have gotten over the years - about $11,000 since 2000 - have been more than negated by inflation.  For instance, the top 1% snagged only 65% of the income gains following the 2001 recession, and just 45% of the income gains after the 1991 recession.

For instance, the top 1% snagged only 65% of the income gains following the 2001 recession, and just 45% of the income gains after the 1991 recession.